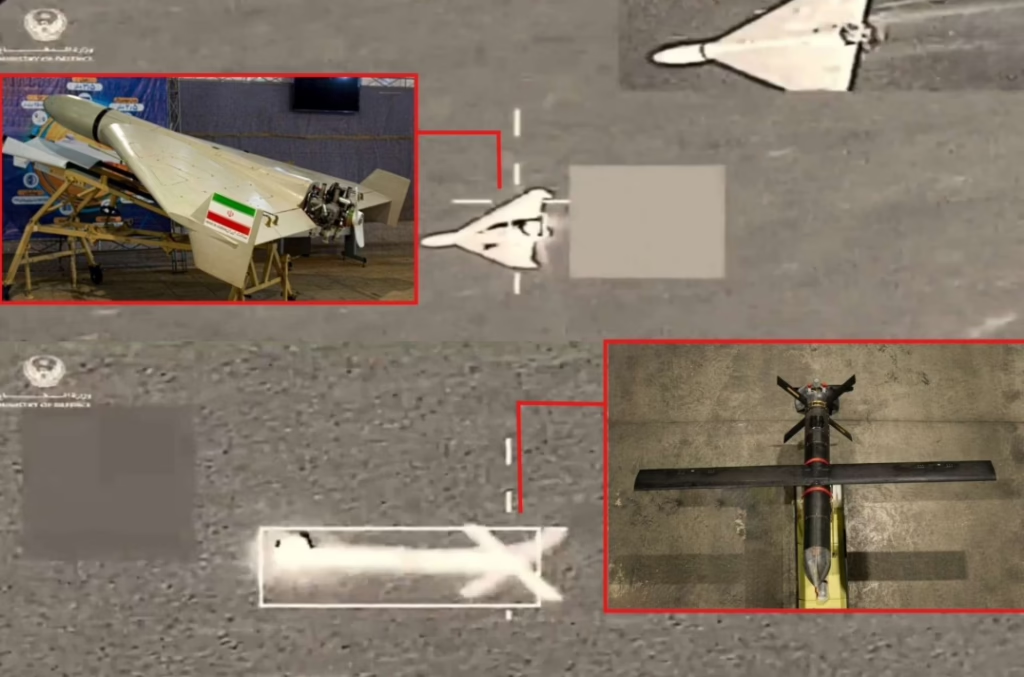

On a single night in late February 2026, Iranian forces launched hundreds of Shahed-136 derivatives toward targets across the Gulf. The UAE alone reported intercepting over 800 drones and ballistic missiles in the opening days of the renewed campaign. Bahrain and Kuwait faced dozens more. Interception rates remained high, yet the sheer volume exposed a familiar strain: traditional air-defense munitions were being expended at unsustainable rates.

This is not an isolated flare-up. It is the latest chapter in a pattern that began years ago in Ukraine and has now spread to Europe and the Middle East. Small unmanned aircraft systems and loitering munitions have turned airspace security into one of the most urgent operational challenges facing the United States and its partners. The cost asymmetry is stark. A $20,000 drone can force the launch of a $2 million missile. When those attacks arrive in swarms or under electronic warfare cover, the math gets worse fast.

The good news is that the United States has finally aligned policy, funding, and operational structure to address this reality. The FY2026 defense budget request dedicates $3.187 billion specifically to counter-unmanned systems programs. When you add interagency grants and state-level initiatives, total U.S. spending on counter-drone capabilities is projected to exceed $4 billion this fiscal year. At the center of the shift sits the newly operational Joint Interagency Task Force 401 (JIATF-401). Standing up its marketplace in February 2026, JIATF-401 now coordinates testing, standards, procurement approvals, and data sharing across DoD, DHS, and DOJ. It has already removed many of the fence-line restrictions that once tied commanders’ hands and has opened faster pathways for contractors to get systems validated and fielded.

This article breaks down exactly where the money is going, which technologies are gaining traction in real operations, and what the combat lessons from Ukraine and the Gulf tell us about the next 12 to 18 months. For intelligence analysts tracking adversary tactics, for policy teams shaping acquisition strategy, and for contractors positioning their portfolios, the message is clear: the window to influence the next generation of counter-drone architecture is open right now.

Table of Contents

The Current Drone Threat Landscape

The February 28, 2026, Iranian barrage marked a new intensity in the ongoing campaign. Over the first week alone, Iranian forces sent hundreds of Shahed-136 derivatives toward targets in the United Arab Emirates, Bahrain, and Kuwait. The UAE reported detecting 941 drones and intercepting 876. Bahrain and Kuwait each faced dozens more in coordinated waves. These numbers reflect the same pattern seen in earlier escalations, but the volume and persistence have grown. Traditional air-defense systems achieved high kill rates yet consumed munitions at a pace that defense planners describe as unsustainable over prolonged periods.

This Gulf reality builds directly on lessons from Ukraine. In 2025 alone, Russia launched more than 54,000 Shahed-type one-way attack drones against Ukrainian cities and infrastructure. Ukrainian forces achieved interception rates of nearly 90 percent in many engagements, but only by combining expensive missiles with low-cost interceptor drones, which now handle roughly 30 percent of all kills.

Europe experienced its own version of this challenge throughout 2025. Unidentified drone flights over military bases in the United Kingdom, Poland, Romania, and the Baltic states increased sharply. In one high-profile case, Copenhagen Airport temporarily closed after multiple incursions near critical airspace. NATO responded by increasing air and maritime patrols in the Baltic Sea and enhancing intelligence sharing among member states.

The threat also crosses into the maritime domain. Repeated incidents involving suspected Russian-linked vessels have damaged undersea data cables in the Baltic and North Sea regions. These events have prompted defense organizations to accelerate work on counter-unmanned underwater vehicles alongside traditional counter-drone programs.

For intelligence analysts, the most important development is the rapid evolution of adversary tactics, techniques, and procedures. Drone operators now integrate small swarms with electronic-warfare jamming to degrade radar and radio links. Some platforms incorporate basic AI autonomy that allows them to continue missions even after losing command links.

Timeline of Major Drone-Related Incidents (2025–Early 2026)

- Late 2025: Sharp rise in unidentified drone sightings over UK and Baltic NATO bases

- December 2025: Copenhagen Airport multiple closures due to drone incursions

- Throughout 2025: Russia exceeds 54,000 Shahed launches against Ukraine

- February 28–March 5, 2026: Iranian Shahed waves target Gulf states (UAE: 941 detected, 876 intercepted)

- Ongoing 2025–2026: Baltic Sea undersea cable sabotage incidents linked to unmanned systems

FY2026 Policy Overhaul and Funding Surge

The Department of Defense has responded to the growing drone threat with one of the clearest signals yet in the FY2026 budget. The request includes $3.187 billion specifically for Counter-Unmanned Systems programs. This represents a $940 million increase over the FY2025 enacted level. When combined with interagency efforts, total U.S. counter-drone spending is on track to surpass $4 billion in fiscal year 2026.

At the center of the new approach stands the Joint Interagency Task Force 401 (JIATF-401). Established in 2025 and now fully operational, JIATF-401 reports directly to the Deputy Secretary of Defense. In late February 2026, JIATF-401 reached initial operational capability for its new Counter-UAS Marketplace. Hosted in the Common Hardware Systems catalog, the platform provides commanders and program offices with a single place to identify, evaluate, and procure validated systems. Early reports indicate the marketplace already contains more than 1,600 tested solutions.

The FY2026 National Defense Authorization Act provided critical legal backing for these changes. It created statutory authority for JIATF-401 and expanded protection authorities for military installations. Commanders now have greater flexibility to operate beyond traditional fence lines when responding to credible threats.

FY2025 vs FY2026 Counter-Unmanned Systems Funding ($ in millions)

| Category | FY2025 Enacted | FY2026 Request | Change |

|---|---|---|---|

| Total DoD C-UXS | 2,247 | 3,187 | +940 |

| Army C-sUAS (procurement + RDT&E) | ~650 | ~858 | +208 |

| Broader U.S. Counter-Drone (incl. interagency) | ~3,100 | >4,000 | +900+ |

Leading Counter-Drone Technologies and Systems

Defense organizations have settled on a layered defense philosophy that matches each stage of a drone threat with the most cost-effective response. Detection comes first through a mix of radar, electro-optical, and radio-frequency sensors. Electronic warfare then provides soft-kill options by disrupting command links or navigation. Kinetic interceptors deliver hard kills when necessary. Directed energy weapons close the sequence with virtually unlimited magazine depth for sustained engagements.

Turkey’s Steel Dome program from ASELSAN stands out for its integrated approach. The system ties together very-short-range to long-range effectors, including KORKUT guns, GÜRZ missiles, SİPER air defense, and İHTAR counter-UAS elements under a single AI-driven command-and-control layer. After its showcase at DIMDEX 2026, Turkey secured $6.5 billion in domestic and export contracts.

The DroneGun Mk4 from DroneShield continues to see strong demand. In the first quarter of 2026 alone, DroneShield announced a $49.6 million European military contract plus an additional $21.7 million in Western orders. More than 4,000 units have now been delivered globally.

Directed-energy weapons have crossed into operational use. Laser systems on the Texas-Mexico border demonstrated successful engagements against drone incursions in early 2026.

Autonomous counter-drone platforms have also advanced rapidly. The Replicator 2 initiative placed its first production buy on the Fortem DroneHunter F700 net-capture system in January 2026.

Key Counter-Drone Systems Comparison (Early 2026 Status)

| System | Primary Effector | Key Strength | Recent Momentum (2026) | Typical Use Case |

|---|---|---|---|---|

| Steel Dome (ASELSAN) | Multi-layer (guns, missiles, EW) | Full-spectrum integration | $6.5B contracts post-DIMDEX | National infrastructure |

| DroneGun Mk4 | RF jamming | Lightweight, portable | $49.6M Europe + $21.7M Western deals | Dismounted and fixed sites |

| Directed Energy (various) | High-energy laser | Unlimited magazine depth | Border ops and Army E-HEL acceleration | Swarm defense |

| Fortem DroneHunter | Net capture (autonomous) | Attritable, low-cost intercept | First Replicator 2 production buy | Mobile maneuver units |

Real-World Combat Lessons and Operational Impact

The Iranian drone campaign that escalated on February 28, 2026, has provided fresh insight into the challenges of countering mass drone attacks. Ukraine has developed the most extensive experience with this type of threat. In February 2026, Ukrainian interceptor drones performed approximately 6,300 sorties and destroyed over 1,500 incoming UAVs. In the Kyiv region, interceptor drones were responsible for more than 70 percent of Shahed kills during the month.

The Ukrainian approach is now attracting attention in the Middle East. President Zelenskyy has offered to send military specialists and interceptor drone operators to assist Gulf states.

The key takeaway from these operations is consistent. Traditional kinetic air defenses struggle to maintain a sustainable cost-exchange ratio against high-volume drone attacks. Successful defense requires a layered strategy that integrates electronic warfare, attritable autonomous interceptors, directed energy weapons, and intelligent command and control.

Remaining Gaps, Challenges, and Subsea Considerations

Despite the substantial new funding and policy reforms, important capability gaps persist. The most pressing operational challenge remains cost sustainability and magazine depth.The integration of subsea threats adds another layer of complexity. Throughout 2025 and into early 2026, the Baltic Sea has seen repeated incidents involving suspected sabotage of undersea data cables. One high-profile case occurred on December 31, 2025, when Finnish authorities seized the cargo ship Fitburg after it dragged its anchor across a fiber-optic cable connecting Helsinki and Tallinn.

The FY2026 NDAA directed reports on low-cost undersea effectors, but dedicated funding and operational concepts remain less mature than their aerial counterparts.

Strategic Outlook and Forecasts for 2027–2030

From 2027 through 2030, counter-drone capabilities will evolve from layered point solutions into fully integrated, software-defined systems that span air, surface, and undersea domains.

Industry analysts project the global counter-UAS market will expand to more than $20 billion by 2030, with a compound annual growth rate of approximately 25 percent.

Autonomous swarm defense networks using low-cost interceptor drones will become standard by 2028. Cognitive electronic warfare systems will gain prominence as adversaries shift to fiber-optic guidance and AI-driven autonomy. Multi-domain counter-unmanned systems will also advance, linking aerial detection and neutralization with underwater effectors.

Final Thoughts

The United States has moved decisively from a reactive posture to a structured, proactive approach to airspace security. The FY2026 budget’s $3.187 billion investment in counter-unmanned systems, combined with the operational launch of JIATF-401 and expanded legal authorities under the NDAA, has created the framework needed to address the cost asymmetry that has defined recent conflicts.

For intelligence analysts, the priority is clear: maintain constant visibility on swarm behaviors, autonomy signatures, and multi-domain TTPs while fully leveraging the new data-sharing channels created by JIATF-401. For contractors, the opportunity window is open today: engage the JIATF-401 marketplace immediately, submit systems for testing, and align development roadmaps with the requirements for software-defined, multi-domain solutions that will dominate through 2030.

The cost curve is finally bending in the defender’s favor. Organizations that act now with speed and precision will help secure that advantage for the next decade.

FAQ

How much is the U.S. Department of Defense spending on counter-drone technologies in FY2026?

The FY2026 budget request allocates $3.187 billion specifically for Counter-Unmanned Systems (C-UXS) programs. Total U.S. counter-drone spending is projected to surpass $4 billion this fiscal year.

What is JIATF-401, and why does it matter for defense professionals?

The Joint Interagency Task Force 401 (JIATF-401) is the new central coordinating body for all Department of Defense counter-small UAS efforts. It runs the Counter-UAS Marketplace (launched February 2026 with over 1,600 validated items).

Which counter-drone systems are seeing the strongest demand and contracts in 2026?

Leading systems include Turkey’s Steel Dome (ASELSAN) with $6.5 billion in new contracts, DroneGun Mk4 (multiple $20+ million deals), high-energy laser platforms, and the Fortem DroneHunter as part of the Replicator 2 initiative.

How are recent Iranian Shahed attacks changing counter-drone strategy?

The February–March 2026 Iranian barrages demonstrated that even high interception rates become unsustainable when large numbers of low-cost drones overwhelm traditional munitions stockpiles.

What combat lessons from Ukraine are most relevant to U.S. and allied forces?

Ukraine achieved roughly 90 percent interception rates in 2025 by shifting to low-cost interceptor drones for the majority of kills (over 70 percent in the Kyiv region in February 2026).

Are there still significant gaps in U.S. counter-drone capabilities?

Yes. The primary challenges remain magazine depth for sustained operations and integration of subsea (C-UUV) threats. The Baltic Sea cable sabotage incidents highlighted the lag in multi-domain capabilities.

How should defense contractors position themselves for FY2026–2027 opportunities?

Focus on systems already validated or in testing through the JIATF-401 marketplace. Priority capability areas include RF/electronic-warfare jammers, directed-energy integration, and affordable attritable interceptors.

What technology trends will dominate counter-drone development from 2027 to 2030?

Expect rapid growth in autonomous swarm defense networks, cognitive electronic warfare, and fully integrated multi-domain systems. The global counter-UAS market is forecasted to reach over $20 billion by 2030.