Picture this. It is 2:17 p.m. on a Tuesday in April 2026. A major prime contractor compliance officer opens an email from DCMA. The subject line reads DFARS Illumination Inquiry Gallium Traceability. The prime contractor 47 million dollar next-gen missile guidance subsystem relies on a Tier 3 supplier in Southeast Asia. That supplier cannot suddenly certify the material origin. The gallium in question now sits on the expanded covered materials list under the FY2026 NDAA.

The prime contractor has 60 days to prove full compliance. Otherwise, it must request a national security waiver. Missing the deadline puts the entire contract line item at risk. This situation could lead to termination for cause. It could also open the door to debarment proceedings. It could even cause an 18-month program delay. Such a delay would cascade through the industrial base.

This scenario is no longer hypothetical. It is happening right now.

The FY2026 National Defense Authorization Act was signed on December 18, 2025. It represents the most aggressive supply chain reset since the original Section 889 Chinese telecommunications ban. Sections 842, 844, 848, 833, 843, and 867 have transformed what used to be best-effort sourcing language into immediate, enforceable obligations.

These obligations come with real teeth.

In the new era of Peace Through Strength procurement, knowing the rules is table stakes. Executing the intelligence that turns those rules into competitive advantage is how programs are won or lost in FY2026 and beyond.

Table of Contents

Timeliness and Enforcement Signals

The FY2026 National Defense Authorization Act took effect on December 18 2025. The Department of Defense has moved quickly to implement it. DFARS updates and interim guidance are already active as of March 2026. This creates immediate obligations for every contractor and subcontractor handling covered materials or advanced batteries.

Enforcement signals are clear and accelerating. The DoD Inspector General and the Defense Contract Management Agency stood up dedicated supply chain compliance task forces in January 2026. These teams have begun issuing preliminary illumination inquiries. The first formal covered materials self-assessments are due to the primes in the second quarter of 2026. Early debarment reviews have already begun for Tier 3 suppliers who failed initial traceability checks.

This timing is not accidental. It aligns directly with the Trump administration’s broader strategy. That strategy includes the February 2026 Critical Minerals Ministerial. It also includes new tariff structures and expansions of Title III of the Defense Production Act aimed at reshoring processing capacity. The administration has made clear that supply chain security is now a core element of the Peace Through Strength industrial policy.

From an intelligence perspective, the enforcement focus will hit Tier 2 and Tier 3 subcontractors hardest first. Primes have received explicit direction to aggressively enforce illumination clauses. This approach means that smaller suppliers face the highest near-term risk. Larger contractors must map their entire supply chains now. Failure to do so will create cascading compliance failures that reach the prime level within months.

These developments explain why the supply chain revolution is exploding in real time. Contractors who treat this moment as an intelligence problem rather than a paperwork exercise will gain a decisive edge in FY2026 awards.

What Actually Changed

The FY2026 NDAA rewrites key parts of the defense supply chain rules. It moves from voluntary efforts to mandatory requirements with clear deadlines and penalties. Four main areas drive the changes. Each one directly affects how contractors source materials and certify compliance starting now.

Covered Materials Expansion (Sections 844 and 848)

The law adds molybdenum, gallium, and germanium to the restricted covered materials list. Any sourcing from China, Russia, Iran, or North Korea now faces a full prohibition. The ban phases in over a five-year period for most materials. New contracts must comply immediately where possible. Existing programs are subject to staged deadlines that culminate in full restriction by 2030. This expands the original Section 889 list and closes previous loopholes for alloy forms and trace elements.

Advanced Batteries and Cells Ban (Section 842)

A strict prohibition targets batteries and cells from Foreign Entities of Concern. The timeline uses three clear cutoffs. New contracts signed after January 1, 2028, cannot use non-compliant batteries. Standard battery programs face restrictions starting in 2029. Legacy programs must convert by 2031. The law includes limited carve-outs for mission-critical systems and a waiver process tied to national security needs. Contractors must document every battery cell supply chain, from raw materials to the final product.

Domestic Preference and Organic Industrial Base Boost (Sections 843, 867, and 832)

Domestic sourcing rules now receive stronger enforcement. Waivers are harmonized across programs and harder to obtain. The Defense Industrial Base Fund gains explicit authority to finance domestic processing and refining capacity. Contested logistics requirements compel contractors to include dual-sourcing plans in all major proposals. These changes give preference to U.S. and allied suppliers in bid evaluations and open new funding pathways for reshoring projects.

Illumination and Transparency Rules (Section 833)

Contractors must now flag any non-compliant items within 60 days of discovery. This applies through mandatory interim national security waiver disclosures. The rule requires detailed traceability reports submitted to the prime or directly to DCMA. False certification carries the same penalties as other DFARS violations, including potential suspension or debarment. This creates a real-time reporting system that replaces earlier vague notification requirements.

The table below shows the practical differences contractors will notice right away.

| Area | Pre 2026 Requirement | FY2026 NDAA Requirement | Effective Date Impact |

|---|---|---|---|

| Covered Materials | Best effort sourcing with limited lists | Expanded list with phased bans on adversary sources | Immediate for new awards; phased to 2030 |

| Advanced Batteries | No specific FEOC prohibition | Three-tier ban timeline with traceability proof | Starts January 2028 for new contracts |

| Domestic Preference | Existing Buy American rules with many waivers | Harmonized waivers and mandatory dual sourcing | Applies to all solicitations now |

| Reporting and Transparency | Voluntary disclosure | Mandatory 60-day illumination and waiver filings | Live in March 2026 |

These provisions shift the burden to contractors to prove compliance at every tier. The next section will examine what this means for different sectors and where the hidden risks lie.

Strategic Winners, Losers, and Hidden Risks

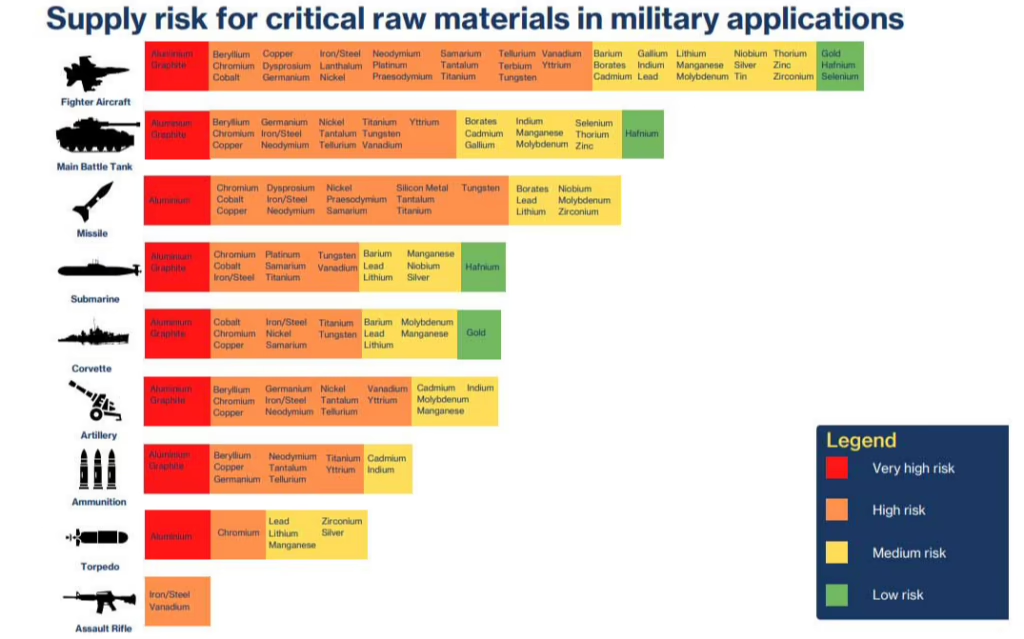

The new rules create clear winners and losers across the defense industrial base. Aerospace and missile programs carry the highest exposure. Gallium and germanium are critical for radar systems, electronic warfare suites, and infrared sensors. Most current supply chains still trace back to Chinese refining. Munitions programs face direct pressure on molybdenum, which is used in kinetic penetrators and hypersonic components. UAS and electric vehicle platforms fall into the highest-risk category due to the advanced battery bans. Ground vehicles remain relatively insulated for now because they rely less on these restricted materials.

Non-traditional suppliers and small businesses with domestic or AUKUS-aligned sourcing now hold a 24 to 36-month golden window. Primes are under pressure to lock in compliant vendors before long-term contracts solidify in 2028. Companies that already invested in U.S. or allied refining capacity can move quickly into teaming arrangements and sole-source opportunities. Traditional Tier 2 suppliers that depend on adversary-sourced trace materials will lose ground unless they reshore fast.

Enforcement patterns point to a focused rollout. Based on past DFARS 252.225 experience, 40 to 60 percent of initial audits will target battery supply chains first. These audits started in Q1 2026 and will expand to covered minerals by late summer. Debarment actions against non-disclosing Tier 3 suppliers are expected to spike in 2027 and 2028. Primes will pass pressure downward through illumination clauses, meaning that smaller subcontractors without strong traceability systems face the greatest near-term risk of contract termination.

China and Russia have already signaled counter moves. Beijing tightened export controls on rare earths in late 2025. Russia restricted exports of nickel and titanium at the same time. These actions point to the accelerated weaponization of critical materials. Contractors should model 30 to 70 percent price spikes in 2027 for gallium, germanium, and molybdenum. Programs that fail to secure alternative sources now will face both compliance failures and sudden cost inflation.

The cost-benefit picture is more favorable than many expect. Initial compliance will raise bill-of-materials costs by 4 to 9 percent over the first 12 to 18 months. That increase buys several long-term advantages. Compliant suppliers gain access to faster award decisions under the new best-value portfolio rules. They also qualify for Defense Industrial Base Fund grants and sole source follow ons. Programs that treat this as a one-time hit rather than a strategic shift will fall behind competitors who use the rules to strengthen their supply base.

The hidden risk lies in the illumination timeline. Many contractors assume they have until the phased ban dates to act. In reality, the 60-day reporting requirement starts now. A single undisclosed non-compliant item discovered during a routine DCMA review can trigger a full program audit. This creates a narrow window in which early movers gain market share while latecomers face cascading delays and lost bids.

This analysis shows the supply chain changes are not just regulatory hurdles. They represent a structural shift that rewards companies with real intelligence on sourcing alternatives and enforcement trends. The next section lays out the exact steps to turn this intelligence into protection for your contracts.

Risk Mitigation Playbook and Exclusive Contractor Checklist

The new rules turn supply chain compliance into a competitive requirement. Contractors who map risks early and act on them will protect their backlog and capture new opportunities. The 10-point checklist below gives you a complete playbook. Each item includes a specific timeline and the owner inside your company who should lead it. Implement these steps in order, and you will stay ahead of DCMA audits and inquiries from the ILL.

Actionable 10 Point Compliance Checklist

- Supply chain mapping audit for gallium germanium, molybdenum, and advanced batteries. Complete this full tier 2 and tier 3 trace in Q2 2026. Assign the supply chain director as the owner.

- Insert illumination reporting clauses in all supplier agreements. Update templates and flow downs by April 30, 2026. Legal counsel owns this step.

- Build a waiver application strategy. Identify when to request national security waivers versus domestic sourcing waivers. Start drafting templates now with the compliance officer in charge.

- Create a domestic and AUKUS sourcing qualification roadmap. Include applications for Defense Industrial Base Fund and IBAS grants. Program managers lead this through Q3 2026.

- Refresh contract language for new RFPs and solicitations. Add traceability and dual sourcing requirements to every proposal. The contracts team owns updates effective immediately.

- Apply a risk scoring matrix to your existing program backlog. Score each line item for exposure and flag high-risk items for mitigation. Finance and compliance teams complete this in May 2026.

- Review insurance and bonding coverage for supply chain disruptions. Adjust policies to cover new compliance-related penalties. The risk management director will handle this review by June 2026.

- Identify and qualify compliant non-traditional suppliers for teaming. Build a short list of domestic or allied sources ready for immediate integration. Business development owns outreach starting now.

- Establish a quarterly self-certification cadence. Set internal audits and reporting deadlines every 90 days. The chief compliance officer leads this ongoing process.

- Define exit ramps if compliance costs exceed 15% of the program margin. Create decision gates and alternative sourcing plans for at-risk programs. Executive leadership reviews these quarterly.

Phased Timeline Overview 2026 to 2031

Use this table as your internal roadmap.

| Period | Key Deadline | Action Required |

|---|---|---|

| March to June 2026 | Illumination reporting live | Mapping audits and clause insertions |

| January 2028 | New contract battery ban begins | Full FEOC compliance for new awards |

| 2029 | Standard battery programs are restricted | Conversion of ongoing production |

| 2030 | Full covered materials prohibition | All sourcing from adversaries ends |

| 2031 | Legacy program conversion deadline | Final cleanup of older systems |

Risk Heat Map by Program Type

This quick reference shows relative exposure levels.

| Program Type | Gallium Germanium Risk | Molybdenum Risk | Battery Risk | Overall Exposure |

|---|---|---|---|---|

| Aerospace Radar EW | High | Medium | Medium | High |

| Munitions Hypersonics | Medium | High | Low | High |

| UAS and EV Platforms | Low | Low | High | High |

| Ground Vehicles | Low | Medium | Medium | Medium |

| Shipbuilding | Low | Low | Low | Low |

These tools and the checklist give you everything needed to turn regulatory pressure into a market advantage. Early movers who complete the mapping audit and secure alternative sources by mid 2026 will see faster awards and stronger negotiating positions with primes.

Forward Looking Intelligence

The supply chain rules in the FY2026 NDAA mark only the beginning of a longer transformation. Defense Department officials and congressional staff have already started drafting language for the FY2027 NDAA. Early indicators suggest further expansion of the list of covered materials. Additional restrictions on rare earth magnets and specialty chemicals are likely. Enforcement mechanisms will likely become stricter, with higher penalties for repeated illumination failures. DFARS cases expected in late 2026 will clarify waiver standards and traceability requirements for alloy forms.

New market opportunities are opening as a direct result of these mandates. Domestic rare-earth processing and refining projects will receive increased funding under the Defense Production Act and the Industrial Base Fund. Battery recycling and second-life applications for defense systems are gaining traction as cost-effective compliance options. Contested logistics technologies that enable rapid shifts in sourcing will see strong demand in major programs.

Companies that position themselves now as reliable domestic or allied suppliers will capture multi-year contracts. The contractors who treat compliance as a strategic investment rather than a cost center will emerge stronger.

Our team is already supporting several prime contractors with supply chain mapping and alternative sourcing strategies. The firms that act in the next six months will define the industrial base for the rest of the decade.

Wrapping Up

The FY2026 NDAA supply chain provisions represent more than regulatory updates. They mark a fundamental restructuring of how the defense industrial base must operate. The combination of expanded covered materials restrictions, strict battery sourcing rules, and mandatory illumination requirements has created a new competitive landscape. Companies that excel at supply chain intelligence will gain clear advantages in the years ahead.

The next 18 months will prove decisive. Contractors who complete comprehensive mapping and secure alternative sources early will build resilient programs. Those who delay will face mounting compliance costs, audit pressure, and reduced competitiveness in major program bids.

This shift rewards strategic foresight over short-term cost savings. The defense contractors that integrate these requirements into their core business strategy, rather than treating them as isolated compliance tasks, will define the next generation of the U.S. defense industrial base.

The intelligence picture is clear. The supply chain revolution is accelerating. Success in this environment belongs to those who act with precision and speed.